Hospital M&A Transactions: A Focus on Retiring Liabilities

The volume of business combinations involving non-profit hospitals is at the highest level of the last decade. The macro-economic forces spurring industry consolidation and rationalization are weighing heavily on management teams and boards around the United States. There is broad consensus that the fragmented ownership structure of the acute-care industry is, in part, responsible for the ineffectiveness of medical outcomes. The presence of a large number of small hospital companies has contributed to the widely held view that our hospital industry, in aggregate, delivers mediocre quality care at an extremely high cost. For these reasons, hospitals are attempting to form larger enterprises to create scale, expand geographically, manage risk, access capital, contend with the changing regulatory environment, improve operating skill, and to more effectively manage the health of the populations they serve.

The volume of business combinations involving non-profit hospitals is at the highest level of the last decade. The macro-economic forces spurring industry consolidation and rationalization are weighing heavily on management teams and boards around the United States. There is broad consensus that the fragmented ownership structure of the acute-care industry is, in part, responsible for the ineffectiveness of medical outcomes. The presence of a large number of small hospital companies has contributed to the widely held view that our hospital industry, in aggregate, delivers mediocre quality care at an extremely high cost. For these reasons, hospitals are attempting to form larger enterprises to create scale, expand geographically, manage risk, access capital, contend with the changing regulatory environment, improve operating skill, and to more effectively manage the health of the populations they serve.

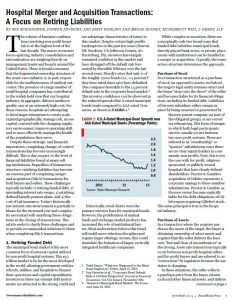

Despite these strategic and financial imperatives, completing change-of-control transactions has become increasingly difficult. This is due, in part, to the level of financial liabilities found at many selling institutions. Regardless of transaction structure, satisfying liabilities has become an onerous part of completing merger and acquisition (M&A) Hospital Merger and Acquisition Transactions- Retiring Liabilities – Oct 2013 transactions for both buyers and sellers. These challenges typically include: 1) retiring funded debt, 2) unwinding interest rate swaps, 3) satisfying defined benefit pension plans, and 4) the cost of tail insurance. Today’s historically low interest rate environment is partially to blame for the increased cost and complexity associated with satisfying these obligations at the closing of transactions. This article seeks to clarify these challenges and to provide recommended solutions to them when completing M&A transactions.