What Will a Trump Presidency Mean for U.S. Healthcare?

By Farley Reardon, Managing Director, Joseph Cerisano, Analyst, and Alexander Norton, Analyst, Juniper Advisory

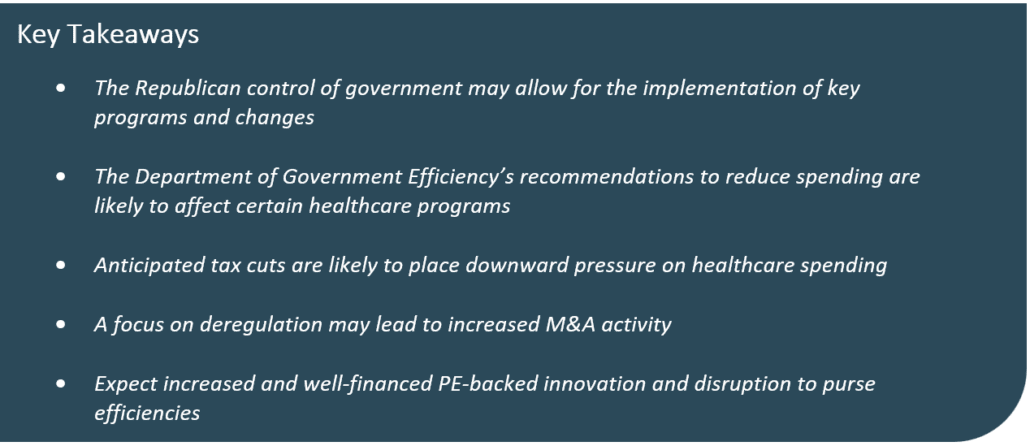

As President-elect Donald Trump prepares to assume office for a second term, again with a Republican majority in both the House and the Senate, healthcare is likely to be an area of focus for policy initiatives, including a focus on spending and deregulation, resulting in required innovation. When introducing the new Department of Government Efficiency (“DOGE”), President-elect Trump described the department as a vehicle to “dismantle Government Bureaucracy, slash excess regulations, cut wasteful expenditures, and restructure Federal Agencies” (NPR). A question for all healthcare leaders is how a reinvigorated Trump White House, coupled with Republican control of the House and the Senate, will impact critical programs in the coming years.

Pursuit of Efficiencies

As introduced, the primary focus of DOGE will be to reduce spending with the benefit of offsetting reduced revenue from anticipated tax cuts. This approach focuses on cost-saving measures, potentially impacting Medicaid supplemental and additional healthcare funding. The stated intent of fostering an environment conducive to economic growth through deregulation and incentivizing innovation is likely to receive a positive reception in Congress.

Reduction in Medicaid Supplemental Funding

According to the Kaiser Family Foundation (KFF), the federal government contributed nearly 70% of total Medicaid spending in 2023 (KFF). With a Republican majority already discussing policies to implement work requirements and introduce block grants or caps on per-enrollee spending, reductions to federal Medicaid funding appear more likely than not. This defined funding structure of block grants or per-enrollee caps, aligns with DOGE’s objective of reducing spending, increasing the likelihood of passage. Analyses highlight that such measures focus on Medicaid as a primary target for spending adjustments to align with broader fiscal priorities (Health Journalism, CBPP). Another area of anticipated reform is with Medicaid work requirements. For states that have implemented such measures, enrollment among non-disabled, working-age adults has declined, resulting in state and federal fiscal savings. While critics have argued that these policies risk limiting access to essential healthcare for vulnerable populations, potentially exacerbating health disparities (CBPP), this is another area where Republican control is likely to facilitate a policy change.

Expiration of Healthcare Extenders

Allowing certain healthcare extender programs to expire, rather than extending the programs for additional terms, represents another avenue for cost savings. Healthcare extender programs refer to programs which receive funding on a temporary basis and require continual reauthorization. Examples include Disproportionate Share Hospital (DSH) payments, which support hospitals and health systems serving high numbers of Medicare and Medicaid patients, and provider reimbursement programs such as physician fee schedules. These constitute significant healthcare expenses at the federal level and require annual spending authorization. Permitting these payments to phase out or reducing funding at renewal would reduce federal spending by billions, without requiring a spending ‘cut’. Proponents of allowing certain programs to sunset argue that reduced government spending on healthcare providers will incentivize hospitals and health systems to adopt more cost-efficient care models while reducing reliance on federal subsidies (Health Journalism). However, the organizations whose revenues are at stake are unlikely to share that view and the American Hospital Association has warned that sunsetting these programs would not require bipartisan legislative action (American Hospital Association).

Before Efficiencies…Medical Debt Collections

Before DOGE recommendations can be finalized or implemented, the Biden White House announced the final rule by the Consumer Financial Protection Bureau (CFPB) to eliminate medical debt from credit reports, which it expects to benefit “…15 million Americans…” with $49 billion in outstanding medical bills remaining on their credit reports (White House). While the CFPB’s authority is likely to change within the new administration, there is no expectation this rule will be overturned. The groups most negatively impacted would be the small and rural healthcare providers, but with many health systems and providers operating at thin margins, it may be the financial tipping point as providers weigh the additional cost for collections against a consumer with no credit score incentive to pay outstanding balances. While typical self-pay revenue represents <5% of the total revenue for a health system, it offsets the cost to hire additional staff and subsidies for critical hospital-based services, invest in new programs, and provide cash flow for future investments. While state and federal programs have provided funds to offset inflation, increasing barriers to collect $49 billion (and rising) for services rendered is another burden on the fragile provider system not likely to be offset by an administration seeking efficiencies.

Deregulation to Promote Free Market Growth

Removing Barriers for Mergers and Acquisitions

Reducing restrictions on merger and acquisition (M&A) activities can facilitate healthcare system consolidation, enabling providers to achieve economies of scale as well as other benefits. Larger healthcare systems often have greater resources to invest in community hospitals, improving access to specialized services such as obstetrics. Consolidated healthcare systems have demonstrated an ability to add essential services in traditionally underserved areas, enhancing care delivery efficiency (Juniper Advisory).

Additionally, consolidation allows healthcare providers to negotiate better terms with vendors, including insurers, reducing overall costs for both patients and the government. Removing barriers to advance M&A activity within reasonable boundaries fosters a competitive, scalable market environment that supports cost-efficient care delivery.

Changes to FTC and Their Impact on M&A

Recent shifts within the Federal Trade Commission (FTC) suggest that the regulatory landscape for mergers and acquisitions (M&A) is poised for meaningful change. The FTC is expected to adopt looser antitrust enforcement policies, particularly in the healthcare sector, compared to the Biden administration. These changes include reversing the revised merger guidelines, which lowered the market share and concentration levels at which at which a merger would be considered illegal (McDermott, Will, & Emery).

Key considerations include proposed updates to merger guidelines to better address the nuances of healthcare transactions and the rising influence of private equity-backed consolidations. Proposed changes by the FTC include refining guidelines to account for industry-specific challenges, such as the unique financial structures and the impact of healthcare consolidation on patient care. Importantly, the FTC’s recent update to Hart-Scott-Rodino (HSR) anti-trust filing guidelines primarily relates to transparency and accountability and does not impact the material decisions on a transaction’s legality. Therefore, experts are not anticipating this to be a focus for President-elect Trump.

Private Equity-Backed Investment

Expanding Reimbursement for Outpatient Service

The continued growth of services provided outside the hospital has attracted private equity-backed competitors and that trend is anticipated to continue under a Trump administration despite increased scrutiny of private equity-backed acute care providers. Besides the direct ambulatory competition, expanding coverage for outpatient services, particularly through ambulatory surgery centers (ASCs), can further reduce the demand for inpatient care. Growth in ASC utilization has been bolstered by the favorable reimbursement policies of both public and private payers. It is unclear whether this shift will receive support from and further accelerate under DOGE, but importantly there have been indications of a reversal.

The CMS 2025 rule updates the Medicare Hospital Outpatient Prospective Payment System (OPPS) and the Ambulatory Surgical Center (ASC) payment systems, adjusting payment rates, improving quality measures, and enhancing access to outpatient services. Notably, it reduces the prior authorization review time from 10 to 7 days and implements add-on payments for expensive drugs used in Indian Health Service facilities. The rule impacts outpatient procedures by enhancing reimbursement rates, refining safety standards, and expanding access, particularly in underserved areas (Holland & Knight), which may lead to additional development in care sites in these communities under the new administration.

Supporting Private Equity-Backed Disruption

Private equity (PE)-backed innovation remains a critical force in reshaping healthcare delivery. Those investing in healthcare include traditional PE firms, including Blackstone, KKR, Thoma Bravo and others, to investment funds established within large, not-for-profit health systems, including Ascension, Intermountain, Northwell and others. Investments in telemedicine, AI-driven diagnostics, and value-based care models are poised to disrupt traditional care systems with the promise of reduced costs. The slow shift from fee-for-service reimbursement to population health models has altered investment dynamics, creating opportunities for PE to invest in companies to enhance efficiency and outcomes (Juniper Advisory).

Other meaningful disruptors include advancements in remote patient monitoring and wearable technology. These innovations enable proactive management of chronic conditions, reducing the need for costly inpatient interventions. Moreover, investments in predictive analytics can help healthcare providers identify at-risk populations, allowing for targeted preventive measures that mitigate long-term expenses. Supporting such innovations aligns with the broader goal of reducing Medicare and Medicaid spending while improving patient outcomes (Health Journalism).

While scrutiny of PE in healthcare has not been limited to the Biden administration, Senator Chuck Grassley’s skepticism being of particular note, FTC Commissioner Lina Khan has been particularly outspoken in challenging the emergence of PE backed healthcare providers, ranging from hospitals to elderly care. She denigrated the private equity model as having “worsened outcomes for workers and patients alike” in a Public Impact Workshop on Private Equity in Healthcare (FTC). While there is general agreement that Khan’s replacement at the FTC, Andrew Ferguson, will loosen merger enforcement, where PE in healthcare will fall out in his priorities remains unknown. That said, the consensus view is that Khan’s concerns relating to “short term, high-risk, and low consequence” ownership models frequently adopted by PE firms operating in the healthcare space are unlikely to be a higher priority for Ferguson than they were for Khan.

Conclusion

In conclusion, the healthcare policy changes anticipated under President-elect Trump’s administration have both potential advantages and drawbacks for healthcare providers. On the positive side, deregulation, including reduced restrictions on mergers and acquisitions, may offer healthcare providers more latitude in how they operate and partner. This can be expected to support cost savings and more efficient care delivery across larger regions and to also help level the balance between payers and providers.

However, traditional providers can also anticipate headwinds. Limiting supplemental funding and introducing work requirements in Medicaid may lead to even larger losses when caring for these populations and potentially exacerbating health disparities. An unresolved issue of how providers will overcome the $49 billion, and likely to increase, of outstanding medical debt is a concern for health systems and President-elect Trump has not indicated that he plans to intervene on the behalf of hospitals.

Overall, sweeping changes appear to be in store across the board as part of DOGE and the new administration with a promise of reducing costs to the federal government, but significant uncertainty on how health systems will be supported. As for changes to healthcare policies and programs, the impact on vulnerable populations and the overall healthcare system will need to be carefully managed to avoid unintended consequences well beyond the next four years.

Full List of Sources Referenced:

1. NPR, Trump appoints Elon Musk to lead so-called ‘DOGE’ with Vivek Ramaswamy. Available at: https://www.npr.org/2024/11/12/g-s1-33972/trump-elon-musk-vivek-ramaswamy-doge-government-efficiency-deep-state

2. KFF, Federal and State Share of Medicaid Spending. Available at: https://www.kff.org/medicaid/state-indicator/federalstate-share-of-spending/?dataView=0¤tTimeframe=0&sortModel=%7B%22colId%22:%22Location%22,%22sort%22:%22asc%22%7D

3. Health Journalism, Deep Cuts in Health Spending Likely Under Second Trump Administration, Experts Say. Available at: https://healthjournalism.org/blog/2024/11/deep-cuts-in-health-spending-likely-under-second-trump-administration-experts-say/

4. CBPP, Trump, Republican Congress Health Care Proposals Could Pose Risks to Access and Affordability. Available at: https://www.cbpp.org/blog/trump-republican-congress-health-care-proposals-could-pose-risks-to-access-and-affordability

5. American Hospital Association, Congress Passes Spending Package on Health Care Extenders. Available at: https://www.aha.org/news/headline/2024-03-11-congress-passes-spending-package-health-care-extenders

6. White House, Fact Sheet: Vice President Harris Announces Final Rule Removing Medical Debt from All Credit Reports. Available at: https://www.whitehouse.gov/briefing-room/statements-releases/2025/01/07/fact-sheet-vice-president-harris-announces-final-rule-removing-medical-debt-from-all-credit-reports/

7. Juniper Advisory, A Glimmer of Hope for Rural Obstetrics. Available at: https://juniperadvisory.com/wp-content/uploads/2023/11/A-Glimmer-of-Hope-for-Rural-Obstetrics_Shields_Webb_Cannon_RrlFcs_Sep2023.pdf

8. McDermott, Will, & Emory, What a Second Trump Term Means for Antitrust Enforcement. Available at: https://www.mwe.com/insights/what-a-second-trump-term-means-for-antitrust-enforcement/#_ftn2

9. Holland & Knight, CMS Releases CY 2025 OPPS and ASC Final Rule. Available at: https://www.hklaw.com/en/insights/publications/2024/11/cms-releases-cy-2025-opps-and-asc-final-rule#:~:text=The%20Centers%20for%20Medicare%20%26%20Medicaid%20Services%20%28CMS%29,%28CMS-1809-FC%29%2C%20which%20updates%20payment%20rates%2C%20policies%20and%20regulations

10. FTC, Remarks by Chair Lina M. Khan as Prepared for Delivery Private Capital, Public Impact Workshop on Private Equity in Healthcare. Available at: https://www.ftc.gov/system/files/ftc_gov/pdf/2024.03.05-chair-khan-remarks-at-the-private-capital-public-impact-workshop-on-private-equity-in-healthcare.pdf

Select Image for Article PDF