Running in Place: The Cycle That Keeps Health Systems from Growing

Adam Davis, Executive Director, Juniper Advisory

Many independent nonprofit health systems and hospitals face a vicious cycle of industry challenges that prevents them from achieving their true growth potential. We call this the “Health System Capital Spending Paradox,” and its manifestation is made possible by strict rating agency criteria and lender covenants that force hospital companies to stockpile cash. The resulting “Liquidity Trap” creates lost opportunities to reinvest in existing capital assets and/or finance strategic projects or acquisitions, thereby stunting growth. Health system executives and Boards need to be aware of this industry dynamic, so they’re prepared to make informed strategic decisions.

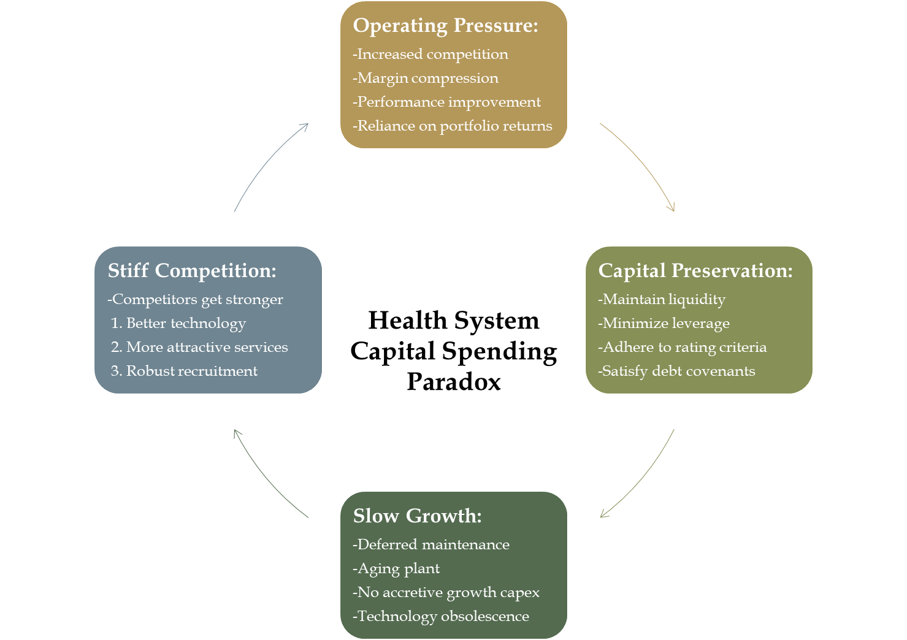

Stage 1: Operating Headwinds

The first stage of the Health System Capital Spending Paradox is when operating performance is weakened by reimbursement challenges, cost pressures and regulatory changes that disproportionately impact independent systems lacking scale, diversification and other resources. Organizations will often respond by implementing intensive performance improvement initiatives to improve profitability and then rely on investment earnings to supplement weak operating cash flow during the turnaround period. Performance improvement efforts can sometimes correct structural issues that allow for a sustainable long-term path forward. However, in many cases these plans just buy time.

Stage 2: Capital Preservation

The second stage of the cycle includes balance sheet protection amid the operating disruptions described in Stage 1. Nonprofit health systems pull back on capital spending to ensure their liquidity ratios (i.e., days cash on hand, debt-to-capitalization) stabilize and thus hoard cash and investments rather than spend them for routine and strategic purposes. They also are motivated to have strong reserves to ensure they generate ample investment returns that support operations. An additional complicating factor is that rating agencies and creditors heavily consider the size of a health system’s cash reserves and leverage position in their assessment of creditworthiness, thereby discouraging capital spending and calculated risk-taking.

Stage 3: Slow Growth

As a result of Stages 1 and 2, nonprofit health systems are motivated to guard their current financial positions rather than augment them. Anemic growth or contraction is often a product of accumulating deferred maintenance and missed opportunities to take advantage of accretive cash flow opportunities.

There’s no clear holistic set of levers that solve each issue and the credit challenges are also circular: if health systems focus on improving operating metrics and preserve cash, they risk underinvestment in existing facilities and therefore will have a higher age of plant.

As mentioned, rating agency criteria and lender covenants restrict health systems from achieving their full potential because of the Liquidity Trap. Juniper estimates that even just deploying 25% of locked up reserves for the average health system can result in age of plant declining by roughly 10% in just the first year with an accretive capital project generating a contribution margin.

Stage 4: Competitive Pressures

In the fourth and final stage, health systems caught in the Health System Capital Spending Paradox will erode their competitive position in the market. They will be at a disadvantage compared to companies with stronger operational capabilities and capacities to invest in innovative services and technology. This is particularly relevant in comparison to for-profits that don’t face the same restrictive rating agency and creditor criteria as nonprofits. In fact, for-profit companies rarely keep any cash reserves on the balance sheet and instead spend them on growth initiatives.

When health systems turn inward, they lose sight of adverse market developments like patient outmigration and weakened relationships with supply chain providers and payors. The recruitment of clinicians, administrators and young talent also becomes challenging if the organization’s reputation and brand are diluted over time.

Coming Full Circle

To summarize the Health System Capital Spending Paradox: 1) Operating headwinds created by industry challenges are addressed often through performance improvement work; 2) As a result of operating issues, capital spending is tightened to preserve balance sheet integrity; 3) The financial position of the organization is stabilized, positioning the organization for more aggressive spending, but 4) Competition stiffens as other nearby organizations invest in growth during the financial stabilization process. Ultimately, the organization finds itself back at Stage 1, where competitive pressures formed in Stage 4 threaten many of the operating improvements and liquidity growth achieved at the start of the cycle.

Can the Cycle be Broken?

Finding an exit ramp is difficult or, in some cases, not feasible. Boards need to assess the long-term sustainability of their health system and make the best fiduciary decisions possible to ensure communities don’t lose services and the organization upholds its mission. Breaking the cycle will require difficult choices that might require significant time and resources. Assessing a holistic range of options is prudent, and considering partnerships with other organizations should be part of that ongoing assessment.