Post-Pandemic Provider Realignment 2.0: If the Past Year Taught Us Anything

By Jordan Shields, Partner, Juniper Advisory, and Brian Fuller, Principal, PYA

Calling 2020 a challenging year for the country as a whole and for providers in particular would be a vast understatement. Disruption reigned across global, national, and local industries.

The healthcare industry found itself at ground zero of the disruption. Extended elective service moratoria, patient reticence to seek treatment, capacity and equipment shortages, staff facing crushing demand and unprecedented risk, and a flood of federal relief funding are but a few of the major, previously unthinkable, products of the pandemic. As we look back, providers have much to be proud of in their resilience and response.

As the pandemic entered the summer of 2020, we authored an article for BoardRoom Press that offered predictions on COVID-19’s effects on provider consolidation.1 Now, nearing 12 months and a seeming lifetime of change later, we believe we are approaching the cusp of the post-pandemic era in U.S. healthcare. As such, it is an appropriate time to revisit those initial predictions, gauge their prescience, and reassess where the industry is and where it is likely going from here.

What Was Right, What Was Wrong, and What Surprised Us

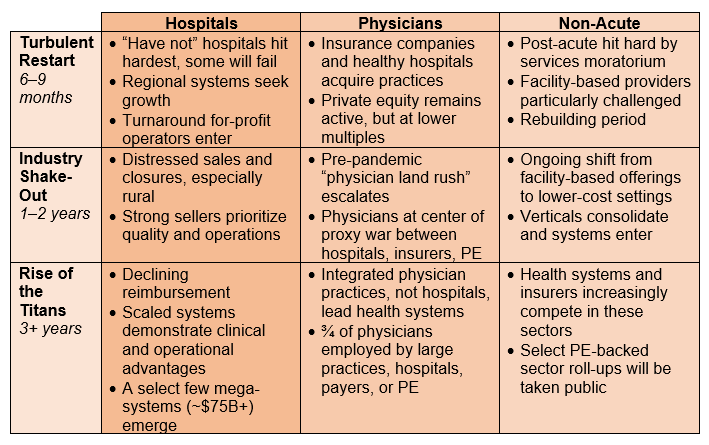

The following table summarizes our June 2020 predictions that were published in BoardRoom Press:

Key Board Takeaways

As boards and senior leadership work to develop or enhance their value-based care delivery strategy, they should:

- Board members must remain acutely and objectively aware of organizational performance, as markets will remain tumultuous over the next five years.

- Population health, anticipated for decades, is finally here. Board members must help determine if their organizations should pursue population health as owners/managers or participants.

- M&A needs to be an intentional element of provider strategic planning. Waiting for the future to present itself is not a strategy.

- Neither consolidation nor status quo guarantees accessible, high-quality, cost-effective care. When considering the future of their organizations, board members must push to understand opportunities, risks, and alternatives.

Looking back on those predictions, it is clear that some proved out, while others were (the authors like to think, anyway!) impossible to forecast.

The Right

Despite two major post-June pandemic surges and their associated disruption, consolidation activity picked back up in the second half of 2020. Led by physician practices, with 208 transactions, the provider sector2 closed 2020 within 10 percent of the number of deals struck in 2019. Hospital transactions were down by about 14 percent.3 When one considers the reality of the pandemic taking up so much organizational focus and energy, this rate is all the more impressive.

Sadly, for many communities, hospital failures also increased in 2020 with bankruptcies up 32 percent.4 Despite the material inflows of relief funding, the challenges of delivering healthcare, especially in rural communities, is proving ever more daunting. Upon reaching the end of relief funds, a major spike in hospital bankruptcies, hitting rural hospitals particularly hard, may be in store.

The Wrong

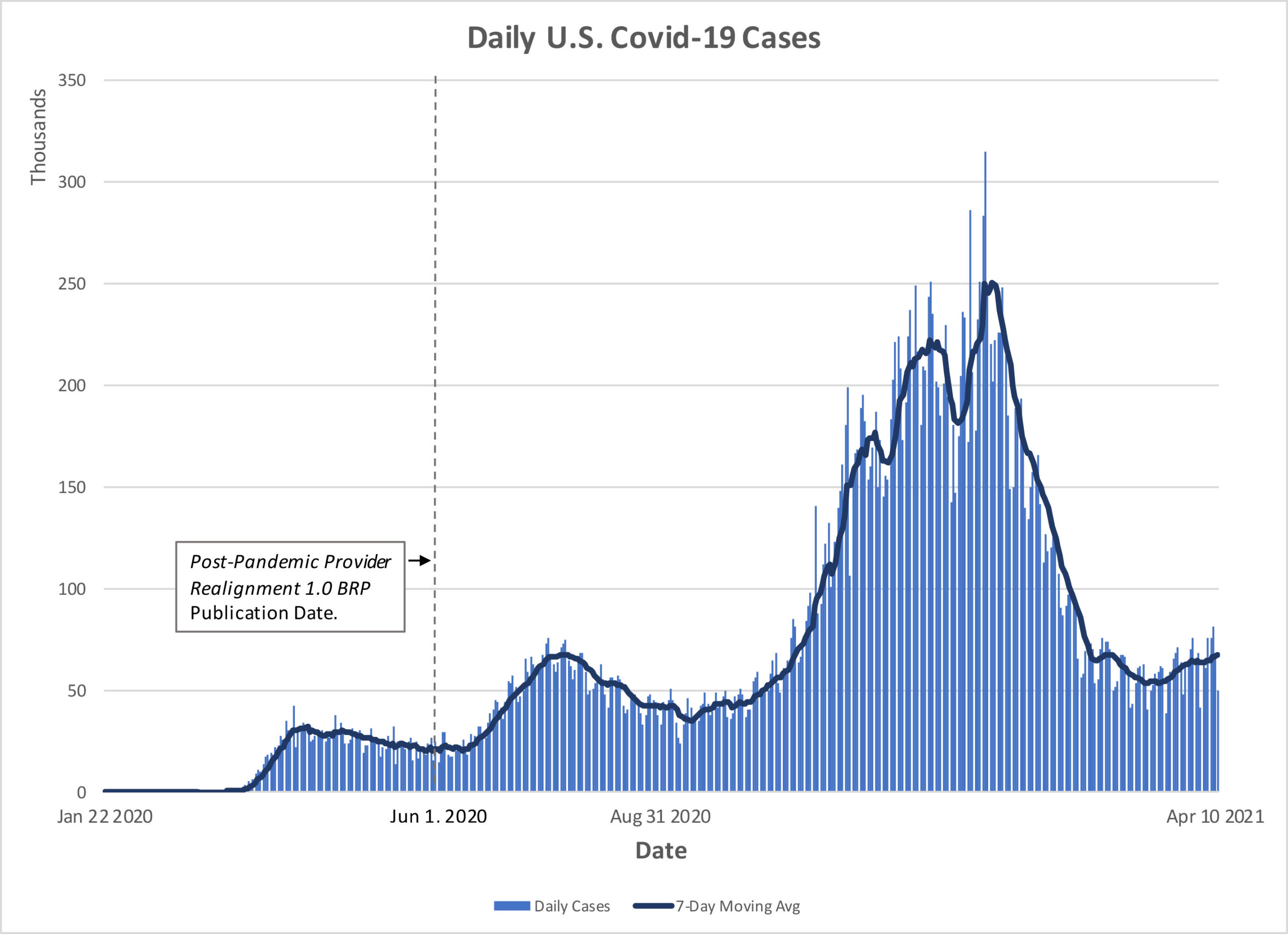

As Exhibit 1 illustrates, we stand guilty of underestimating the pandemic’s staying power. While we considered June the industry’s effective restart date, the pandemic had other ideas.

As a result of the pandemic’s persistence, it is likely the industry still finds itself in the “turbulent restart” phase. Despite that reality, however, the number of transactions in an uncertain 2020 demonstrated a significant appetite for growth across sectors.

The Surprises

We did see an uptick in distressed transactions, but a wholesale “rush to the exits” in acutely challenged sectors never emerged. This was particularly noticeable among physicians. While many practices transacted in 2020, even more, in our experience, continued to pursue their independent growth strategies. Between the loosening of telehealth payment rules and the injection of significant relief funding into the sector, operations were buoyed, and practices made deliberate decisions to hold on and not to sell amidst the uncertainty, and depressed valuations, of the pandemic.

Looking Ahead: 2021 and Beyond

With the increasing clarity of our post-pandemic future emerging, we believe a number of issues will drive provider activity going forward, including:

- “Hardening” of the business model: Providers will move to minimize fee-for-service payment risk through aggressive pursuit of population health strategies, leading to:

- Increased participation in risk-based payment arrangements

- Continued investment in clinical and operating efficiency, through care and cost management, respectively

- Pursuit of growth to access attributed lives and offer comprehensive delivery networks

- Ascendance of access as a differentiator: The pandemic provided a peek into a future of “disperse demand” that will advantage those that can deliver care across locations, platforms, and channels.

The rebasing of provider competition around networks, risk, and access will advantage the scaled, and serve as the rationale for continued industry consolidation across provider sectors well into the next decade. As distance between the pandemic and the industry grows, boards need to be asking their management teams the pace at which these phenomena are affecting their markets, as well as management’s plans for addressing them.

1. Acceleration of the “Have and Have Not” Phenomenon

The pandemic took an outsized toll on under-capitalized hospitals, though the impact was blunted by emergency federal and state aid. Regardless of the amount of aid, there was a 32 percent increase in bankruptcies and distressed sales in 2020. As we proceed through 2021 and beyond, under-capitalized facilities, especially those in rural areas, will continue to face mounting pressure. We do not anticipate that pressure subsiding.

Meanwhile, large, well-capitalized health systems have performed at record profit levels, despite elective procedure and other utilization drop-offs. While we expect margin compression across the industry as relief funding ends and governmental payers seek to rein in costs, systems that can demonstrate efficiency and that have the resources for continued investment will thrive and grow. This will further the divide in the nation’s hospital sector.

2. Mega-Systems Are Coming

The 2020 prediction that received the most debate, the rise of $75-billion+ mega-systems, remains on the medium-term horizon as we exit the pandemic. We still consider the arrival of these mega-systems a virtual certainty. Growth will come both in geographic expansion and acute-care acquisitions, as well as investments in care integration, like physicians, post-acute services, community health, and more.

To be clear, we are not predicting the end of stand-alone providers or that a handful of systems will own all hospitals and physician practices. On the hospital side, small organizations will need to run faster to keep up, but well-positioned independent organizations will find ways to compete, often through partnerships and contractual affiliations that do not require a change of ownership. Among physicians, we are already seeing groups make investments to create lower-cost ambulatory health networks in a bid to outrun large systems.

3. Value Propositions Matter More than Ever

While we firmly believe health systems will grow materially over the coming decade, we were reminded in the last 12 months of the importance of the value proposition—simple, credible, quantified—as the critical underpinning of successful growth by acquisition. As combinations grow larger, complexity multiplies, losing sight of (or lacking) clear and quantifiable reasoning behind their pursuit is a sure path to failure.

The list of 2020 “pulled” mergers, those that would have served as the cornerstones of the mega-systems described above, was long and full of notable names. While the announcements confirm the desire of the country’s largest systems to continue growing, the failures underline the complexity in doing so. In this environment, board members must be willing to challenge conventional wisdom and assumptions, push management teams to quantify value, and, most certainly, demonstrate cultural fit.

4. The Physician “Land Rush” will Recommence…Led by Insurers

Despite the pandemic, physician practices transacted at impressive rates in 2020 and that trend appears to be accelerating in 2021. While acquirers will come from many corners—hospitals, second generation physician management companies, and private equity—we expect the insurers to continue leading the pack. We think this trend deserves mention, in part, because of how insurers have been talking about these investments as licensed-based vs. market-based. Insurers are already leveraging physicians to deliver telemedicine services, often in locations far from the doctor’s office. We expect that trend to continue and, with it, pressure on imaging, laboratory, proceduralist, inpatient service, and other costs.

While we believe physician practice consolidation will increase, we are not spelling the end of the independent practice of medicine. 2020 found large primary care and multi-specialty groups learning a lot about their critical importance to their markets, their ability to shift business models to truly manage care and overcome market disruption. Heavily capitated primary care groups, in particular, reported less financial disruption, as revenue continued to arrive regardless of patient volume levels. At the same time, multi-specialty groups with significant investments in primary care found themselves capable of pivoting quickly into telehealth, frequently going from zero to thousands of virtual visits per week, seemingly overnight. We expect these groups to vigorously pursue their own growth prior to considering consolidation going forward.

What’s Next?

Historians will view the COVID-19 pandemic as a great accelerator of change in U.S. healthcare, but not change’s root cause. The industry’s ails, apparent for decades, lacked a catalyst for change. In COVID-19, and its fundamental disruption to the healthcare business model, that catalyst has arrived. If one looks to industry reactions throughout 2020 and into 2021, it is clear that M&A will be a material tool in industry re-imagination and re-creation. The reshaping of the provider industry, underway prior to the pandemic, has reached an inflection point.

The Governance Institute thanks Jordan Shields, Partner, Juniper Advisory LLC, and Brian Fuller, Principal, PYA, P.C., for contributing this article. They can be reached at jshields@juniperadvisory.com and bfuller@pyapc.com. The authors would like to thank Alexandra Normington, Director of Communications, Juniper Advisory LLC, and Corbin Brown, Consulting Intern, PYA, P.C. for their contributions to this article.

1 Jordan Shields and Brian Fuller, “Provider Realignment Post-Pandemic,” BoardRoom Press, The Governance Institute, June 2020.

2 Defined as physician practices and services and hospitals/health systems sectors.

3 Kaufman Hall, 2020 M&A in Review: COVID-19 as Catalyst for Transformation.

4 Ayla Ellison, “22 Hospital Bankruptcies in 2019,” Becker’s Healthcare, January 6, 2020; Ayla Ellison, “29 Hospital Bankruptcies in 2020,” Becker’s Healthcare, June 3, 2020.